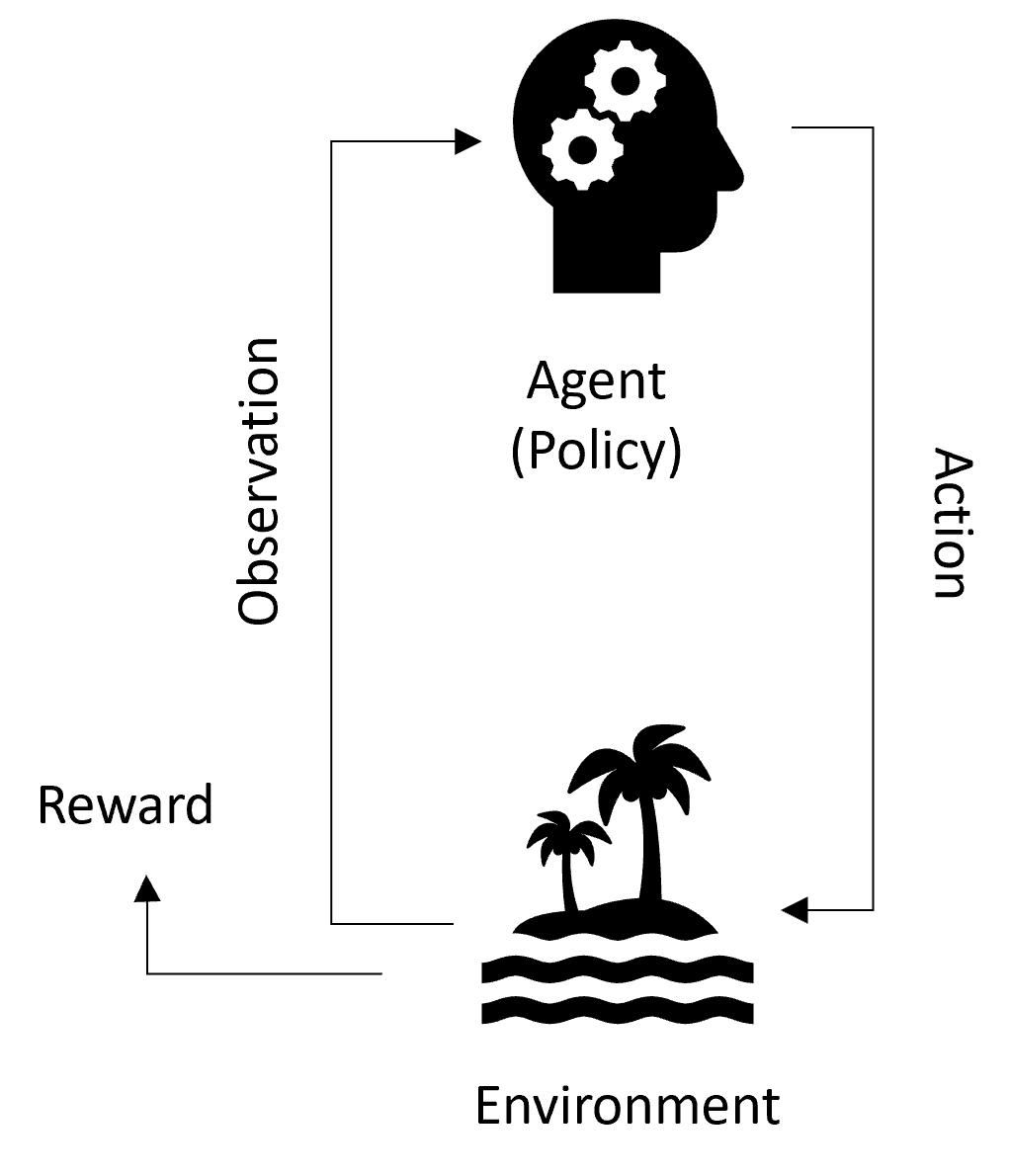

Simulation Loop

The simulation loop in dojo brings everything together through an iterative process on a per block basis.

At each step the environment emits an observation and the agents' rewards. These are processed by the policy which generates a sequence of actions. This is passed to the environment, which emits a new observation reflecting the new state of the protocol, and the agents' rewards for taking those actions.

Basic Pattern

This is the basic pattern of the simulation loop:

- Firstly, the environment emits an initial observation to the agent, which represents the state of the environment.

- Then the agent takes in the observations and makes decisions based on its policy. It also computes its reward based on observations.

- If you are testing your strategy, this reward is simply a way of measuring your strategy performance.

- The environment executes the actions and moves forward in time to the next block.

- The simulation loop keeps repeating this cycle until it reaches the end block.

If you want a reminder on some of the concepts here, take a longer peek at the environment, the agent or the policy as you see fit.

Example

pools = ["USDC/WETH-0.05"]

start_time = "2024-12-06 13:00:00"

chain = Chain.ETHEREUM

block_range = (

time_to_block(start_time, chain),

time_to_block(start_time, chain) + num_sim_blocks,

)

# block_range = 21303933, 21354333

market_agent = HistoricReplayAgent(

chain=chain, pools=pools, block_range=block_range

)

# Agents

trader_agent = TotalWealthAgent(

initial_portfolio={

"ETH": Decimal(100),

"USDC": Decimal(10_000),

"WETH": Decimal(100),

},

name="TraderAgent",

unit_token="USDC",

policy=MovingAveragePolicy(

pool="USDC/WETH-0.05", short_window=25, long_window=100

),

)

lp_agent = TotalWealthAgent(

initial_portfolio={"USDC": Decimal(10_000), "WETH": Decimal(100)},

name="LPAgent",

unit_token="USDC",

policy=PassiveConcentratedLP(lower_price_bound=0.95, upper_price_bound=1.05),

)

# Simulation environment (Uniswap V3)

env = UniswapV3Env(

chain=chain,

block_range=block_range,

agents=[market_agent, trader_agent, lp_agent],

# agents=[market_agent],

pools=pools,

backend_type="local",

)

# SNIPPET 2 START

backtest_run(

env,

dashboard_server_port=dashboard_server_port,

auto_close=auto_close,

simulation_status_bar=simulation_status_bar,

output_file="example_backtest.db",

simulation_title="Example backtest",

simulation_description="Example backtest. One LP agent, one trader agent.",

)

# SNIPPET 2 ENDThis is a visualization of the above simulation:

Saving data

One way to store data is through the dashboard. The dashboard allows you to save all data in JSON format on a per block basis. You can load it into an empty dashboard later, or read the JSON for further processing. You can also turn a db file produced by your simulation directly into JSON format by using `dojo.external_data_providers.exports.json_convertor. Consult the documentation for more details.